Private Equity 20 Lectures (14) Private equity fund equalization successive two

Private Equity 20 Lectures, Silicon Valley Investors' Legal Requirements, I am American lawyer Liu Xiaoxiao.

In a previous issue, we introduced Capital Call/Drawdown and realized that Capital Call/Drawdown can be divided into many times. But similarly, Capital Commitment/Subscription can also be divided into batches, especially in larger funds, in the first one or two years of limited partners (Limited Partner/LP) to come in one after another, there may be the first delivery (First Closing) and the second delivery (Second Closing), then there will be the first delivery (First Closing) and the second delivery (Second Closing). Under such circumstances, how to balance the distribution of interests between First Closing and Second Closing? In this issue, we will introduce the equalization of private equity funds.

After the General Partner (GP) obtains a sufficient Capital Commitment to launch the fund, a Private Placement Memorandum (PPM) is issued stating the First Closing date of the fund. The PPM will be issued to indicate the First Closing date of the fund, before which the Limited Partners/LPs can complete their paperwork and Capital Call/Drawdown.

However, after the First Closing, the General Partner/GP can still seek additional investments, i.e., additional Limited Partners/LPs, under the terms specified in the Private Placement Memorandum (PPM). These additional investments are called Subsequent Closing. A Subsequent Closing is any closing that occurs after the Initial Closing, either from a Subsequent Investor or a Subsequent Capital Commitment from an Existing Investor. Subsequent Capital Commitments from Subsequent Investors and Subsequent Capital Commitments from Existing Investors, which need to be equalized.

The concept sounds simple, but with different investors joining the fund at different dates, the allocation of Limited Partners (LPs) is a problem. In practice, most private equity funds perform equalization when recruiting new Limited Partners/LPs.

So what is equalization?

Let's take an example.

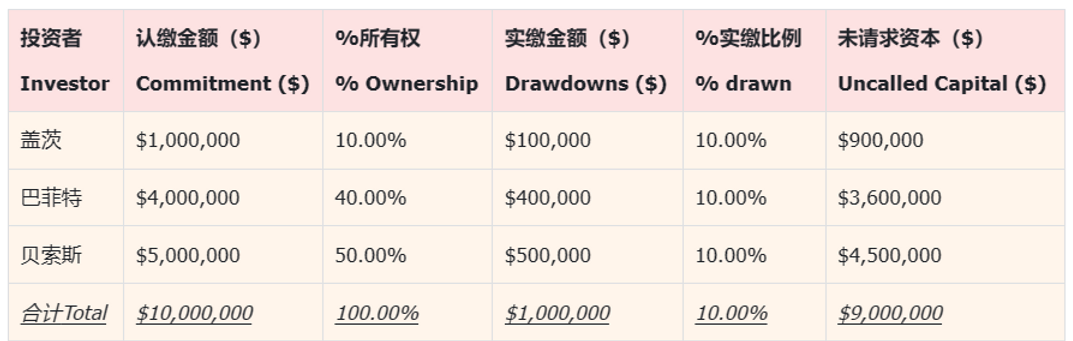

Let's say that Incep Venture Fund starts with a $10m Initial Closing, Gates contributes $1m, Buffett contributes $4m, Bezos contributes $5m, and a Capital Call is made for $1m. Incep Venture Fund's capital structure is now as follows:

*** Translated with www.DeepL.com/Translator (free version) ***

Incep Venture Fund has made a Second Closing in which Musk, the Subsequent Investor, made a Capital Commitment of $2.5m to Incep Venture Fund.

The capital structure of Incep Venture Fund is now as follows:

But that seems a bit off, because Gates, Buffett and Bezos have already paid down (Drawdown) 10% of their Subscription, while Musk hasn't paid down (Drawdown) anything yet!

You might think, "How easy can it be? Let Musk make a 10% Capital Call, that is, pay $0.25m to balance. However, having just invested in a project, Incep Venture Fund does not have any new projects to invest in right now, and putting $0.25m into the fund's bank account will only result in a lower IRR for Incep Venture Fund's fund, and the General Partner/GP will have to pay $0.25m to the Limited Partners at the end of the year. This will only lead to a decrease in IRR of Incep Venture Fund, which will make it difficult for the General Partner/GP to report to the Limited Partner/LP at the end of the year.

This is where Equalization comes into play, Equalization is the process of adjusting all Limited Partners (Limited Partner/LP), and the result of the adjustment is as if Subsequent Investors (Subsequent Investor) had joined the fund before the date of First Closing (First Closing), just as Subsequent Investors (Subsequent Investor) had joined the fund before the date of First Closing (First Closing). The result is as if the Subsequent Investor had joined the fund prior to the First Closing date.

Equalization is generally divided into two steps: Equalization Capital and Equalization Interest.

1. Equalization Capital

Specific operation is: we let Musk paid (Drawdown) his share of $ 1m, that is, $ 0.2m (($ 10m * 10%) / ($ 2,500,000 / $ 12,500,000) = $ 0.2m), after the transfer out of what? Instead of putting it into the fund's bank account, it is returned to the Limited Partner/LP who made the First Closing. That is, as shown in the figure below: Musk will distribute his own $0.2m to other Limited Partners/LPs to achieve equalization (Equalization). So you can see that a fund would rather return money than have cash lying around in the fund's bank account in order to preserve its Internal Rate of Return (IRR).

2. Equalization Interest

But that's not all. Since Musk joins on the Second Closing, we need him to compensate the Initial Investor for the interest, which is often called Equalization Interest.

How is Equalization Interest calculated?

Equalization Interest is generally calculated based on the length of time between the Divestment and Subsequent Closing, and the interest rate is set by the Limited Partnership Agreement (LPA). --The interest rate is set by the Limited Partnership Agreement (LPA) - usually the Market Rate plus a number of Basis Points, or the 8% Minimum Interest Rate.

Let's say our fund charges new Limited Partners/LPs 8% per year as Equalization Interest. Then, Musk will have to pay 8% interest on the amount ($0.2m) that should have been paid in the First Closing but was paid in the Second Closing, that is, ($0.2m)*(8%)*(1/4)=$4,000, and distribute this $4,000 interest pro rata amongst the Initial Investors (Intial). Investor) between the proportionate distribution, equivalent to Musk and the first few Limited Partner (Limited Partner/LP) first borrowed money for 3 months.

The calculations we've just described may seem relatively simple, but they are already highly abstracted and simplified data, and the actual calculations can be complex as other factors multiply. It may be necessary to track multiple Capital Calls between Initial Closing and Subsequent Closing, as well as multiple Equalizations with different investors at different times. Not to mention the fact that there are often several sub-funds under one fund, and the General Partner/GP needs to keep track of the details of multiple funds at the same time.

Private Equity 20 Lectures, a legal must for Silicon Valley investors, I'm Xiaoxiao Liu, a U.S. attorney.