Silicon Valley Legal Bible (22)Ten Years of Unicorn Documentation

In our previous episode, we introduced Unicorns and their extended family: Decacorns, Hectocorns, Soonicorns, and Minicorns. When the term “Unicorn” was first coined in 2013, there were only 39 such companies. In just a decade, that number exploded to over 1,200. Yet since 2022, Unicorns have begun collapsing en masse, morphing into Brokencorns—so much so that even Aileen Lee, the venture capitalist who popularized the term, has grown skeptical of its relevance.

How are Unicorns forged?

Why did they sprout multiple horns (becoming Decacorns and Hectocorns) only to break them overnight? And does the Unicorn label still hold weight in tomorrow’s venture capital world? Let’s dissect the decade of the Unicorn.

The 42-Chapter Silicon Valley Codex

A legal encyclopedia tailored for founders.

I’m Liu Xiaoxiao, a U.S. attorney in Silicon Valley. Stay tuned for the analysis.

1. The Original 39 Unicorns

In 2013, when Aileen Lee first introduced the term “Unicorn”, the U.S. had just 39 companies on its Unicorn list. Among them were now-household names like Facebook, Uber, YouTube, Twitter, LinkedIn, Dropbox, Airbnb, and Evernote.

Think of these 39 as the "first Ivy League" of startups—their early inclusion in the Unicorn club carried first-mover prestige, much like China’s inaugural "985" universities in higher education. Over time, however, the exclusivity diluted as the list expanded, turning what was once a gold standard into a more commonplace designation.

2. 2021: The Year of the Unicorn Explosion

Indeed, since 2013, Unicorns have exploded in number—transforming from rare, serendipitous discoveries (with just a few emerging annually) into a mass-produced commodity, averaging one new Unicorn per day.

It’s akin to the shift from star athletes scouted for raw talent to idols factory-made by talent agencies—a transition from organic rarity to industrialized scale.

As this chart reveals:

Pre-2013, Unicorns were sparse anomalies.

Post-2013, their emergence became exponentially dense—eventually clustering into an indistinguishable blur.

Was Aileen Lee prophetic, coining the term Unicorn just before its explosive rise? Or did her 2013 conceptualization itself ignite startups’ frenzy to chase the $1B valuation badge? Aileen Lee and the Unicorn—which created which?

Regardless, once the “Unicorn” benchmark was set, “$1 billion valuation” became the singular metric of startup success. Here’s the paradox:

Without a standard, we crave one.

With a standard, achieving it often renders the pursuit hollow.

Today, there are over 1,200 Unicorns globally—a 31x increase since 2013. The year 2021 alone saw 622 new Unicorns (half of today’s total), marking it as the “Year of the Unicorn Explosion.”

Whether in China or the U.S., Unicorns typically take 5-8 years to mature, with 7 years being the average.

However, some companies sprinted to Unicorn status in record time:

Hopin (a virtual events platform) and Bird (e-scooter sharing) hit $1 billion USD in just one year.

Fair (car leasing) reached the milestone in two years.

Convoy (trucking logistics) and Knotel (flexible workspace) took three years.

But here’s the kicker: These “Unicorn crash-course graduates”—companies that peaked at launch—all collapsed into Brokencorns.

3. 93% of Unicorns Are Papercorns

In the era of Unicorn mass production, the venture capital world has awakened to the flaws.

Aileen Lee, the original architect of the Unicorn concept, now warns:

93% of Unicorns are “Papercorns” (companies inflated by hype, not substance),

60% are “ZIRPcorns” (products of the Zero Interest Rate Policy bubble).

This “star-making frenzy” is unraveling. But how did so many gilded shells with hollow cores rise and fall so rapidly?

3.1 Inflation

Following the 2008 financial crisis, a decade of inflation eroded the U.S. dollar’s purchasing power. You might argue: “But inflation rates and the dollar’s value appear relatively stable!”

Inflation primarily reflects consumer-side data, such as the cost of daily goods and services. However, its impact is even more pronounced on the asset side.

In an inflationary environment, investors tend to allocate funds to physical assets or inflation-hedging instruments to counteract the erosion of currency value. As a result, asset prices rise significantly faster than consumer prices.

For example, since 2008:

U.S. home prices have shown a steep upward trend, especially in first-tier cities like New York, San Francisco, and Los Angeles.

The NASDAQ index has also surged, reflecting the rapid growth of tech-driven assets.

The stock market’s trajectory is even more telling:

Pre-2008 financial crisis: Growth was steady and gradual.

Post-2008: It skyrocketed, fueled by quantitative easing and low interest rates.

This bull run created a wealth effect, where inflated stock prices spilled over into private markets, driving up startup valuations.

Another critical factor driving this phenomenon is prolonged low interest rates.

3.2 Low Interest Rates

Interest rates represent the cost of borrowing money, while asset prices reflect how much money an asset can fetch. The relationship between the two is inverse:

Lower interest rates = Higher asset prices.

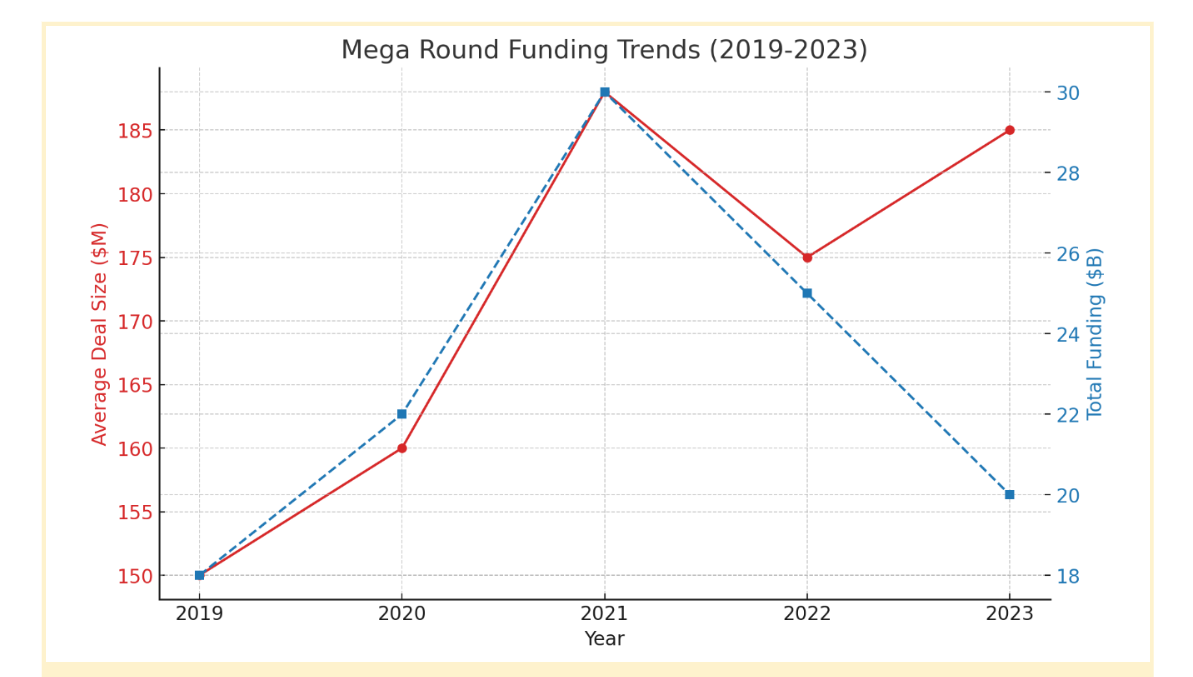

In the era of prolonged low rates, investors scrambled to deploy capital rather than hold cash. 2021, marked by ultra-loose monetary policy, saw venture capital funding hit record highs, with Mega Rounds (investments exceeding $100 million) becoming commonplace.

In this environment, a flood of “ZIRPcorns” emerged—Unicorns born under the Zero Interest Rate Policy (ZIRP).

As the chart below shows, 2021, the year with the lowest interest rates, also saw the highest number of Unicorn coronations.

Today, 60% of Unicorns are “ZIRPcorns”—companies inflated by cheap capital during the ZIRP era.

But as the Federal Reserve began raising interest rates in March 2022, the valuation bubble started to burst. These ZIRPcorns, once soaring in the clouds, are now crashing back to earth.

The pace of Unicorn creation has also slowed significantly.

As the chart illustrates:

2021 saw a sharp peak in Unicorn births,

But by Q2 2022, the trend began to decline.

3.3 Extended Time in the Primary Market

While inflation and low interest rates contributed to soaring valuations, they alone can’t explain how companies reached $1 billion+ valuations in under a decade. A more direct factor: today’s venture capitalists prefer keeping startups in the primary market longer.

What does this mean?

A decade or two ago, if a company could IPO in 5 years, private investors wouldn’t wait 10 years. If it could IPO in 3 years, they wouldn’t wait 5.

Back then, investors pushed for early IPOs, moving companies to the secondary market to tap public investor funds.

Today’s approach is different:

Investors now aim to prolong startups’ stay in the primary market, relying more on private capital.

Why? A company’s hypergrowth phase typically lasts 10 years, after which growth plateaus. By capturing this golden decade, private investors can maximize returns.

Did past investors not understand this? Of course they did. But achieving “longer primary market stays” required specific enabling conditions.

3.4 Wealth Inequality

One enabling condition is widening wealth inequality. Today, wealth is concentrated in the hands of a few high-net-worth individuals, while the middle class has less disposable income.

This ties back to what I mentioned earlier: the secondary market’s influence has weakened. Why?

The middle class primarily engages in the secondary market (e.g., stock trading).

Private equity investments, however, are the domain of high-net-worth individuals, who operate in the primary market.

This shift explains why, in major cities, people are no longer rushing to buy property or trade stocks. Instead, private equity investments are becoming increasingly common.

Thus, the strategy of keeping startups in the primary market longer has gained economic feasibility.

3.5 The 2012 JOBS Act

Another key factor is the 2012 JOBS Act, which raised the maximum number of shareholders for private companies from 500 to 2,000.

What does this mean?

Before 2012, private companies with over 500 shareholders faced public company-level compliance and disclosure requirements, prompting many to opt for an IPO.

Post-2012, private companies can have up to 2,000 shareholders without meeting these stringent requirements, allowing them to stay in the primary market longer with fewer regulatory burdens.

4. What’s Next for Unicorns?

In this evolving landscape, does the Unicorn label still hold value?

Think of it like this: top students will always have value, but high grades alone don’t guarantee a successful career or life. Similarly, in today’s market—where investors are smarter, capital bubbles are shrinking, and rationality prevails—chasing sky-high valuations no longer works.

The focus must shift to building solid, sustainable businesses.

The 42-Chapter Silicon Valley Legal Bible

A legal encyclopedia tailored for founders.

I’m Liu Xiaoxiao, a U.S. attorney in Silicon Valley. See you next time.