Private Equity 20 Lectures (9) "Subscription" and "Drawdow" in private equity, Capital Call

Private Equity 20 lectures, Silicon Valley investors must study the law, I am the American lawyer Liu Xiaoxiao.

Anyone who has been in the VC circle must have often heard fund managers say the word Capital Call, which is directly translated as "Capital Call", which sounds like some kind of magical spell, but in order to use a more neutral term, we usually translate it as "Capital Request", and sometimes it is also called "Drawdown". For the sake of using a more neutral terminology we usually translate it as "Capital Call", sometimes it is also called Drawdown. Speaking of Capital Call (Capital Request), we have to talk about Capital Commitments (Capital Commitments), sometimes also called Subscription (Subscription), what does it mean? You can roughly classify these two concepts as Contributions and Actual Contributions respectively in the Chinese context.

Capital Commitments/Subscription

Capital call/Drawdown

The main reason why these two concepts exist is because LPs in a fund usually don't have that much cash on hand at once, and even the richest people don't save all their money in the bank. Moreover, it takes several years for a venture capital fund to gradually invest in the right project company, so it is not necessary to get all the LP's investment immediately.

I. The case step-by-step explanation

Let's take an example to illustrate it!

First Capital Call

For example, there is an Incep Venture Fund, the fund's Total Asset Management (Total Asset Management) is $ 100m, specializing in the field of artificial intelligence investment, and recently is planning to make a startup XYZGPT $ 5m A round of investment, but the fund's current account is only about $ 1m. To carry out the transaction, we need to raise another $ 4m from the LP. To do the deal, we need to raise another $4m from the LP. This is where a Capital Call comes in. We have 80 LPs in the fund with contributions ranging from $100,000 to $10m.

The current Subscription, Drawdown and Usage Status of the fund is shown below:

Usually when GP makes a capital call, it is done in proportion to the LPs' contributions, otherwise if there are 80 LPs and GP only makes a capital call from 20 of them, then these 20 LPs will suspect that GP is only taking money from their 20 LPs but giving the proceeds to all 80 LPs, that will be impossible to agree because the Total Asset Management is $100m. It is impossible to agree to this because the Total Asset Management of the fund is $100m, and if you want to get $5m, then each LP has to contribute 5% of the Capital Commitments, which is the amount of the Capital Call.

In order to avoid repeated Capital Calls to LPs, the GP will usually make more calls at once, so the GP actually notifies the LPs that it has made a 10% call. For example, an LP that has made a Capital Commitment of $1m, the American Librarians Pension Fund wired $100,000 (10% of $1m) to complete a Capital Call. Similarly, the other LPs are legally obligated to pay their pro rata share, which is 10% of their respective capital commitments.

So let's look at the Subscription, Drawdown and Usage Status at this point.

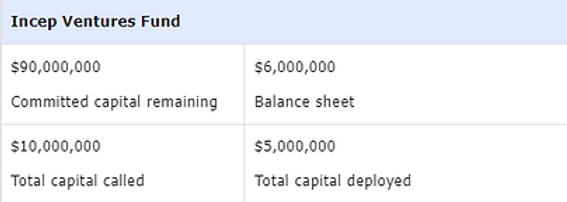

$10m of the Total Asset Management of $100m has been called, leaving $90m of Capital Commitment. There was only $1m in the bank account and now there is $11m, but no funds have been used yet.

Following the completion of the $5m transaction with XYZGPT, the status of the Fund's subscriptions, payouts and use of funds is as follows.

The fund still has a Capital Commitment of $90m that can be called in the future, and there is $6m in the bank.

Second Capital Call

Two months later, Incep Venture Fund had another $10m Series B investment in an AI company called Future.AI, and only had $6m left in the bank account, so it was time for another Capital Caital.

Or every time will generally call more, originally $10m in $100m accounted for 10%, but GP to LP notice is 15%. That means the American Librarian Retirement Fund remitted another $150,000, and other LPS followed suit, remitting 15% of their Capital Commitment.

At this time, the fund's account balance increased to $21m, of which $10m was wired to Future.AI to complete the Series A transaction, and the bank account balance was $11m.

After two such Capital Caital (Capital Request), the fund still has $ 75m Capital Commitment (Capital Commitment) can be used for subsequent calls, while the account also has enough cash to carry out other negotiations on several small investments.

II. Capital Call (Capital Call) two major strategies

Capital Call (Capital Call) is not used casually, the formulation of Capital Call (Capital Call) is important to consider the timing and is the amount, in short, is the time and money.

Timing of Capital Call

If we withdraw capital before a deal is finalized but the deal doesn't work out, the money from the Capital Call will remain in the fund's account, dragging down two important measures of fund performance:

Fund Internal Rate of Return (IRR)

Total Value to Paid-in Capital (TVPI)

I won't explain these two concepts in detail, but they are both used to measure the performance of the fund, and they are both calculated using the actual Capital Call (Capital Request) out of the money as the denominator, so obviously the GP wants the Capital Call (Capital Request) out of the money as little as possible.

So what should we do?

Typically, a seasoned GP will informally notify his limited partner LPs as soon as he begins discussing investing in a company to ensure that the subsequent Capital Call is not too sudden. It usually takes 10 to 14 days for the LP to remit the money.

As we have just seen, GPs generally call out a little more when making a Capital Call because they want to minimize the number of Capital Calls. On the one hand, the management cost is also higher, especially for funds with a large scale of capital management and a large number of LPs, to contact all of them, the fund managers under the GP will have to make hundreds of phone calls. On the other hand, LP is not necessarily free, venture capital trading process is a race against time, only to ten days of time window, that LP is not sitting there every day waiting for you to contact, today this closed practice, tomorrow the family dead, the day after tomorrow and then one to the national forest park inside the no signal.

But the one-time Capital Call (capital request) can not be too much, why? On the one hand, from the LP's point of view, they may not be able to come up with too much cash in a short time, and we should know that the 2% fixed management fee of the fund is based on the amount of the actual Capital Call, so LPs also hope that the Capital Call will happen as late as possible, and call as much as possible. On the other hand, from the GP's point of view, the GP doesn't want to leave too much money in the fund account, because it will lower the IRR (internal rate of return) and make the GP's year-end report to the LP's data very difficult to see.

Therefore, the timing and amount of Capital Call (capital request) is very difficult to pinpoint. As a result, in the last decade or so, many private equity funds have begun to use capital call lines of credit to ensure that they have the necessary funds on hand to complete the transaction. A capital call line of credit is a short-term loan from a third party that can be used to invest in a company while waiting for the LP to transfer funds. In this way, the LP saves on management fees on the one hand, because the GP holds the capital for a shorter period of time and can legitimately increase the IRR (internal rate of return) of the fund.

III. Liability for LP's failure to fulfill Capital Call payment obligations

Generally, LPs rarely fail to fulfill Capital Call because the circle of private equity funds is very small, and this situation will spread very quickly, so that GPs of other funds will not dare to accept the investment of the defaulting LP. But defaults can happen, and what happens when an LP defaults depends on the Limited Partner Agreement. According to the Limited Partner Agreements we've read, usually the GP can:

GPs use their own money to invest first, charging LPs a penalty of a few percentage points per day.

Kick the LP out of the fund. You can see how severe the penalties are in the case of an LP defaulting on a Capital Call.

In this issue, we are talking about how Capital Call/Drawdown can be divided into many parts. But similarly, Capital Commitments/subscriptions can also be divided into batches, especially for larger funds, where LPs come in one by one in the first one or two years, and there may be First Closing and Second Closing, so how to balance the First Closing and the Second Closing under such a situation? In this case, how to balance the distribution of interests between First Closing and Second Closing? In the next issue, we will introduce the equalization of private equity funds.

Private equity fund 20 lectures, Silicon Valley investors' legal must study, I am the U.S. attorney Liu Xiaoxiao.